电子商务运营师考试

淘宝网直通车广告属于下面哪一种形式()A、CPC(COST PER CLICK)B、CPS(COST PER SALES)C、CPA(COST PER ACTION)D、CPM(COST PER MILLE)

题目

淘宝网直通车广告属于下面哪一种形式()

- A、CPC(COST PER CLICK)

- B、CPS(COST PER SALES)

- C、CPA(COST PER ACTION)

- D、CPM(COST PER MILLE)

相似问题和答案

第1题:

(b) Using the information contained in Appendix 1.1, discuss the financial performance of HLP and MAS,

incorporating details of the following in your discussion:

(i) Overall client fees (total and per consultation)

(ii) Advisory protection scheme consultation ‘utilisation levels’ for both property and commercial clients

(iii) Cost/expense levels. (10 marks)

(ii) As far as annual agreements relating to property work are concerned, HLP had a take up rate of 82·5% whereas MAS

had a take up rate of only 50%. Therefore, HLP has ‘lost out’ to competitor MAS in relative financial terms as regards

the ‘take-up’ of consultations relating to property work. This is because both HLP and MAS received an annual fee from

each property client irrespective of the number of consultations given. MAS should therefore have had a better profit

margin from this area of business than HLP. However, the extent to which HLP has ‘lost out’ cannot be quantified since

we would need to know the variable costs per consultation and this detail is not available. What we do know is that

HLP earned actual revenue per effective consultation amounting to £90·90 whereas the budgeted revenue per

consultation amounted to £100. MAS earned £120 per effective consultation.

The same picture emerges from annual agreements relating to commercial work. HLP had a budgeted take up rate of

50%, however the actual take up rate during the period was 90%. MAS had an actual take up rate of 50%. The actual

revenue per effective consultation earned by HLP amounted to £167 whereas the budgeted revenue per consultation

amounted to £300. MAS earned £250 per effective consultation.

There could possibly be an upside to this situation for HLP in that it might be the case that the uptake of 90% of

consultations without further charge by clients holding annual agreements in respect of commercial work might be

indicative of a high level of customer satisfaction. It could on the other hand be indicative of a mindset which says ‘I

have already paid for these consultations therefore I am going to request them’.

(iii) Budgeted and actual salaries in HLP were £50,000 per annum, per advisor. Two additional advisors were employed

during the year in order to provide consultations in respect of commercial work. MAS paid a salary of £60,000 to each

advisor which is 20% higher than the salary of £50,000 paid to each advisor by HLP. Perhaps this is indicative that

the advisors employed by MAS are more experienced and/or better qualified than those employed by HLP.

HLP paid indemnity insurance of £250,000 which is £150,000 (150%) more than the amount of £100,000 paid by

MAS. This excess cost may well have arisen as a consequence of successful claims against HLP for negligence in

undertaking commercial work. It would be interesting to know whether HLP had been the subject of any successful

claims for negligent work during recent years as premiums invariably reflect the claims history of a business. Rather

worrying is the fact that HLP was subject to three such claims during the year ended 31 May 2007.

Significant subcontract costs were incurred by HLP during the year probably in an attempt to satisfy demand and retain

the goodwill of its clients. HLP incurred subcontract costs in respect of commercial properties which totalled £144,000.

These consultations earned revenue amounting to (320 x £150) = £48,000, hence a loss of £96,000 was incurred

in this area of the business.

HLP also paid £300,000 for 600 subcontract consultations in respect of litigation work. These consultations earned

revenue amounting to (600 x £250) = £150,000, hence a loss of £150,000 was incurred in this area of the business.

In contrast, MAS paid £7,000 for 20 subcontract consultations in respect of commercial work and an identical amount

for 20 subcontract consultations in respect of litigation work. These consultations earned revenue amounting to

20 x (£150 + £200) =£7,000. Therefore, a loss of only £7,000 was incurred in respect of subcontract consultations

by MAS.

Other operating expenses were budgeted at 53·0% of sales revenue. The actual level incurred was 40·7% of sales

revenue. The fixed/variable split of such costs is not given but it may well be the case that the fall in this percentage is

due to good cost control by HLP. However, it might simply be the case that the original budget was flawed. Competitor

MAS would appear to have a slightly superior cost structure to that of HLP since its other operating expenses amounted

to 38·4% of sales revenue. Further information is required in order to draw firmer conclusions regarding cost control

within both businesses.

第2题:

A、10

B、100

C、1000

D、1000

第3题:

A.10

B.100

C.1000

D.1000

第4题:

N Company manufactures a kind of product used throughout the machinery industry.The standard price of the materials for the products is $ 6 per kilogram; the standard quantity of materials allowed per unit is 1.5 kilograms. During July, 2 000 units of the products were finished, for which 3 200 kilograms of materials were used at a total direct material cost of $ 18 560.

Requirment :

A. Calculate the direct material price variance for July. Indicate whether it is favorable (F) or unfavorable (U) and who is generally responsible for this variance.

B. Calculate the direct material quantity variance for July. Indicate whether it is favorable (F) or unfavorable (U) and who is generally responsible for this variance.

C. Calculate the total direct material cost variance for July. Indicate whether it is favorable (F) or unfavorable (U).

Answer:

A. Direct material price variance

= Actual quantity*( actual price - standard price)

=3 200 * (18 560/3 200 -6)

=3 200* (5. 8 -6)

= -640 (F)

Purchasing department

B. Direct material quantity variance= Standard price * ( actual quantity - standard quantity)=6 *(3 200 -2 000 *1.5)= $1 200 (U)

Manufacturing department

C. Total direct material cost variance

= Direct material price variance + Direct material quantity variance

=1 200 - 640 = $ 560 (U)

or = Actual cost - Standard cost

=18 560 - (1. 5*6*2 000)

=$560(U)

第5题:

KFP Co, a company listed on a major stock market, is looking at its cost of capital as it prepares to make a bid to buy a rival unlisted company, NGN. Both companies are in the same business sector. Financial information on KFP Co and NGN is as follows:

NGN has a cost of equity of 12% per year and has maintained a dividend payout ratio of 45% for several years. The current earnings per share of the company is 80c per share and its earnings have grown at an average rate of 4·5% per year in recent years.

The ex div share price of KFP Co is $4·20 per share and it has an equity beta of 1·2. The 7% bonds of the company are trading on an ex interest basis at $94·74 per $100 bond. The price/earnings ratio of KFP Co is eight times.

The directors of KFP Co believe a cash offer for the shares of NGN would have the best chance of success. It has been suggested that a cash offer could be financed by debt.

Required:

(a) Calculate the weighted average cost of capital of KFP Co on a market value weighted basis. (10 marks)

(b) Calculate the total value of the target company, NGN, using the following valuation methods:

(i) Price/earnings ratio method, using the price/earnings ratio of KFP Co; and

(ii) Dividend growth model. (6 marks)

(c) Discuss the relationship between capital structure and weighted average cost of capital, and comment on

the suggestion that debt could be used to finance a cash offer for NGN. (9 marks)

(b)(i)Price/earningsratiomethodEarningspershareofNGN=80cpersharePrice/earningsratioofKFPCo=8SharepriceofNGN=80x8=640cor$6·40NumberofordinarysharesofNGN=5/0·5=10millionsharesValueofNGN=6·40x10m=$64millionHowever,itcanbearguedthatareductionintheappliedprice/earningsratioisneededasNGNisunlistedandthereforeitssharesaremoredifficulttobuyandsellthanthoseofalistedcompanysuchasKFPCo.Ifwereducetheappliedprice/earningsratioby10%(othersimilarpercentagereductionswouldbeacceptable),itbecomes7·2timesandthevalueofNGNwouldbe(80/100)x7·2x10m=$57·6million(ii)DividendgrowthmodelDividendpershareofNGN=80cx0·45=36cpershareSincethepayoutratiohasbeenmaintainedforseveralyears,recentearningsgrowthisthesameasrecentdividendgrowth,i.e.4·5%.Assumingthatthisdividendgrowthcontinuesinthefuture,thefuturedividendgrowthratewillbe4·5%.Sharepricefromdividendgrowthmodel=(36x1·045)/(0·12–0·045)=502cor$5·02ValueofNGN=5·02x10m=$50·2million(c)Adiscussionofcapitalstructurecouldstartfromrecognisingthatequityismoreexpensivethandebtbecauseoftherelativeriskofthetwosourcesoffinance.Equityisriskierthandebtandsoequityismoreexpensivethandebt.Thisdoesnotdependonthetaxefficiencyofdebt,sincewecanassumethatnotaxesexist.Wecanalsoassumethatasacompanygearsup,itreplacesequitywithdebt.Thismeansthatthecompany’scapitalbaseremainsconstantanditsweightedaveragecostofcapital(WACC)isnotaffectedbyincreasinginvestment.Thetraditionalviewofcapitalstructureassumesanon-linearrelationshipbetweenthecostofequityandfinancialrisk.Asacompanygearsup,thereisinitiallyverylittleincreaseinthecostofequityandtheWACCdecreasesbecausethecostofdebtislessthanthecostofequity.Apointisreached,however,wherethecostofequityrisesataratethatexceedsthereductioneffectofcheaperdebtandtheWACCstartstoincrease.Inthetraditionalview,therefore,aminimumWACCexistsand,asaresult,amaximumvalueofthecompanyarises.ModiglianiandMillerassumedaperfectcapitalmarketandalinearrelationshipbetweenthecostofequityandfinancialrisk.Theyarguedthat,asacompanygearedup,thecostofequityincreasedataratethatexactlycancelledoutthereductioneffectofcheaperdebt.WACCwasthereforeconstantatalllevelsofgearingandnooptimalcapitalstructure,wherethevalueofthecompanywasatamaximum,couldbefound.Itwasarguedthattheno-taxassumptionmadebyModiglianiandMillerwasunrealistic,sinceintherealworldinterestpaymentswereanallowableexpenseincalculatingtaxableprofitandsotheeffectivecostofdebtwasreducedbyitstaxefficiency.Theyrevisedtheirmodeltoincludethistaxeffectandshowedthat,asaresult,theWACCdecreasedinalinearfashionasacompanygearedup.Thevalueofthecompanyincreasedbythevalueofthe‘taxshield’andanoptimalcapitalstructurewouldresultbygearingupasmuchaspossible.Itwaspointedoutthatmarketimperfectionsassociatedwithhighlevelsofgearing,suchasbankruptcyriskandagencycosts,wouldlimittheextenttowhichacompanycouldgearup.Inpractice,therefore,itappearsthatcompaniescanreducetheirWACCbyincreasinggearing,whileavoidingthefinancialdistressthatcanariseathighlevelsofgearing.Ithasfurtherbeensuggestedthatcompanieschoosethesourceoffinancewhich,foronereasonoranother,iseasiestforthemtoaccess(peckingordertheory).Thisresultsinaninitialpreferenceforretainedearnings,followedbyapreferencefordebtbeforeturningtoequity.TheviewsuggeststhatcompaniesmaynotinpracticeseektominimisetheirWACC(andconsequentlymaximisecompanyvalueandshareholderwealth).TurningtothesuggestionthatdebtcouldbeusedtofinanceacashbidforNGN,thecurrentandpostacquisitioncapitalstructuresandtheirrelativegearinglevelsshouldbeconsidered,aswellastheamountofdebtfinancethatwouldbeneeded.Earliercalculationssuggestthatatleast$58mwouldbeneeded,ignoringanypremiumpaidtopersuadetargetcompanyshareholderstoselltheirshares.Thecurrentdebt/equityratioofKFPCois60%(15m/25m).Thedebtofthecompanywouldincreaseby$58minordertofinancethebidandbyafurther$20maftertheacquisition,duetotakingontheexistingdebtofNGN,givingatotalof$93m.Ignoringotherfactors,thegearingwouldincreaseto372%(93m/25m).KFPCowouldneedtoconsiderhowitcouldservicethisdangerouslyhighlevelofgearinganddealwiththesignificantriskofbankruptcythatitmightcreate.ItwouldalsoneedtoconsiderwhetherthebenefitsarisingfromtheacquisitionofNGNwouldcompensateforthesignificantincreaseinfinancialriskandbankruptcyriskresultingfromusingdebtfinance.

第6题:

Christopher bought 4 cans of soup for a total of $3.36,which included sales tax of $0.16. At the same per-can cost, what is the cost before the sales tax is added for 6 cans of the same soup?

A.$0.80

B.$0.84

C.$4.80

D.$5.04

E.$6.40

第7题:

A、10

B、100

C、1000

D、1000

第8题:

(d) Calculate the ex dividend share price predicted by the dividend growth model and discuss the company’s

view that share price growth of at least 8% per year would result from expanding into the retail camera

market. Assume a cost of equity capital of 11% per year. (6 marks)

(d) The dividend growth model calculates the ex div share price from knowledge of the cost of equity capital, the expected growth

rate in dividends and the current dividend per share (or next year’s dividend per share). Using the formula given in the

formulae sheet, the dividend growth rate expected by the company of 8% per year and the decreased dividend of 7·5p per

share:

Share price = (7·5 x 1·08)/(0·11 – 0·08) = 270p or £2·70

This is the same as the share price prior to the announcement (£2·70) and so if dividend growth of 8% per year is achieved,

the dividend growth model forecasts zero share price growth. The share price growth claim made by the company regarding

expansion into the retail camera market cannot therefore be substantiated.

In fact, a lower future share price of £2·49 was predicted by applying the current price-earnings ratio to the earnings per

share resulting from the proposed expansion. If this estimate is correct, a fall in share price of 7% can be expected.

The share price predicted by the dividend growth model of £2·70 would require an after-tax return on the proposed expansion

of 11·66%, which is more than the 9% predicted by the Board. The current return on shareholders’ funds is 7·5% (4·5/60),

but in 2005 it was 12·8% (7·3/57), so 11·66% may be achievable, but looks unlikely.

Since the market price fell from £2·70 to £2·45 following the announcement, it appears that the market does not believe

that the forecast dividend growth can be achieved.

第9题:

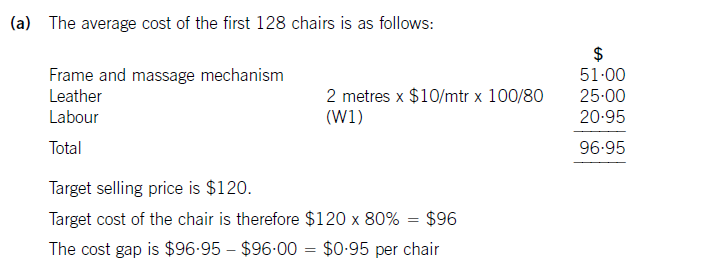

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

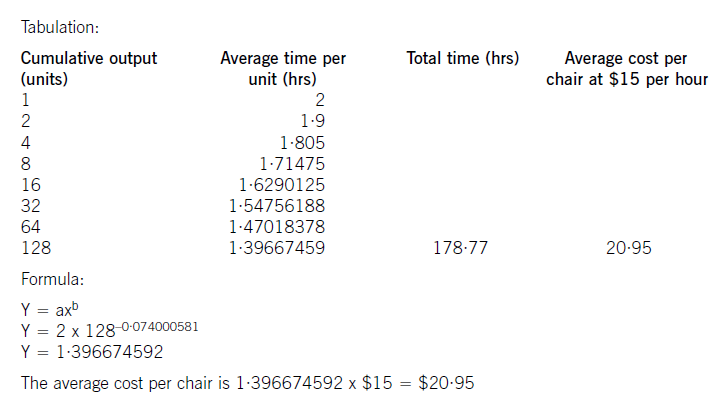

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

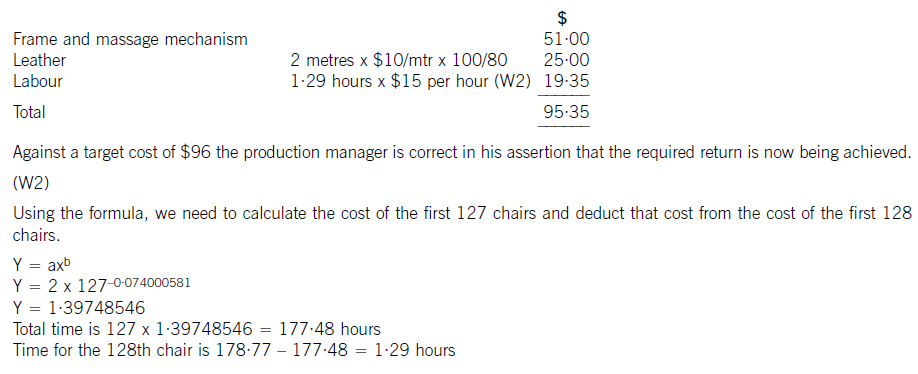

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

第10题:

淘宝网站广告属于下面()形式?

- A、CPC(COSTPERCLICK)

- B、CPS(COSTPERSALES)

- C、CPA(COSTPERACTION)

- D、CPM(COSTPERMILLE.

正确答案:A